Auto insurance can feel confusing when you first start looking at policies, deductibles, coverage limits, and insurance terms. But at its core, auto insurance exists for one main reason:

It helps protect drivers financially after accidents, vehicle damage, injuries, theft, or other covered events.

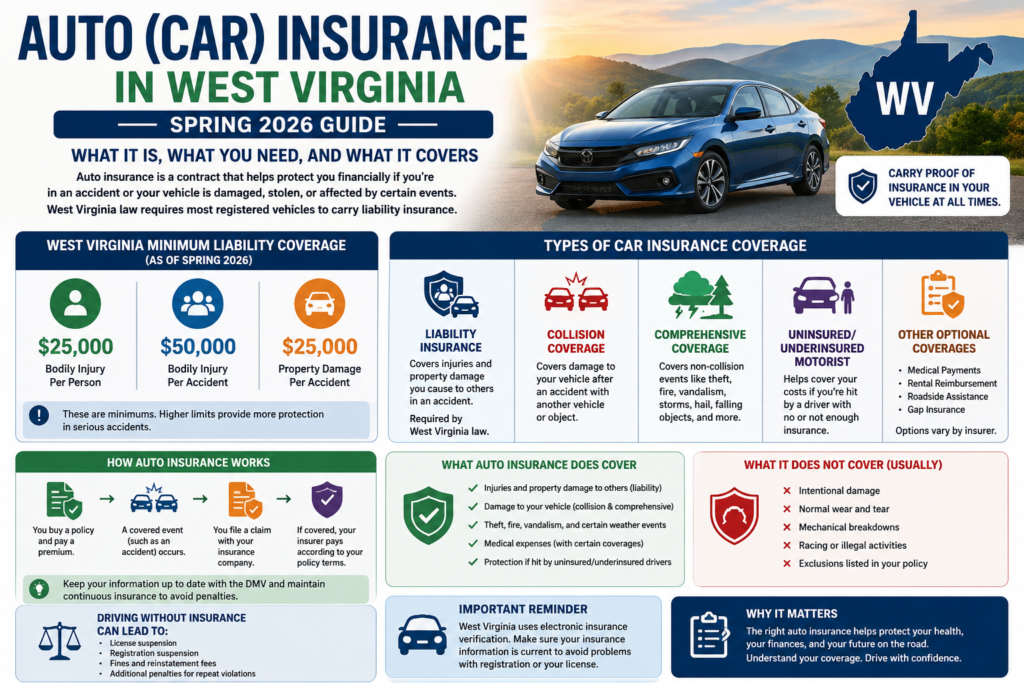

In West Virginia, auto insurance is also required by law for most registered vehicles. Driving without insurance can lead to license suspensions, registration issues, fines, and other penalties.

This guide explains:

- What auto insurance is

- The main types of coverage

- Minimum West Virginia requirements

- What “full coverage” actually means

- What insurance usually covers — and what it doesn’t

- Common mistakes drivers make

What Is Auto Insurance?

Auto insurance is a contract between you and an insurance company.

You pay a monthly or yearly premium, and in exchange, the insurance company may help pay for certain losses involving your vehicle, injuries, or property damage after covered events.

Depending on your policy, auto insurance may help pay for:

- Damage to vehicles

- Medical expenses

- Property damage

- Legal liability

- Theft

- Storm damage

- Injuries caused by uninsured drivers

Different policies provide different levels of protection.

Some cover only the minimum required by law. Others provide broader financial protection.

Is Car Insurance Required in West Virginia?

Yes.

West Virginia law requires registered vehicles to carry liability insurance issued by a company licensed in the state. Drivers are also required to carry proof of insurance in their vehicle.

As of Spring 2026, West Virginia’s minimum required liability coverage includes:

- $25,000 for bodily injury to one person

- $50,000 for bodily injury per accident

- $25,000 for property damage

You may sometimes see these limits written as:

25 / 50 / 25

That shorthand refers to:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $25,000 property damage

These are only minimums. Many drivers choose higher limits for additional protection.

The Main Types of Car Insurance

Liability Insurance

Liability insurance helps cover damage or injuries you cause to other people if you are at fault in an accident.

This is the core coverage required by West Virginia law.

Liability insurance is generally divided into two categories:

Bodily Injury Liability

May help pay for:

- Medical bills

- Lost wages

- Pain and suffering claims

- Legal expenses

Property Damage Liability

May help pay for:

- Damage to another vehicle

- Fences

- Buildings

- Mailboxes

- Other damaged property

Important:

Liability insurance usually does not pay for damage to your own vehicle.

Collision Coverage

Collision coverage may help repair or replace your own vehicle after an accident involving:

- Another vehicle

- A pole

- A guardrail

- A tree

- A rollover

- Other collisions

Collision coverage can apply regardless of fault, depending on the policy and deductible.

If you finance or lease a vehicle, lenders often require collision coverage.

Comprehensive Coverage

Comprehensive insurance covers many non-collision events.

This may include:

- Theft

- Fire

- Vandalism

- Storm damage

- Falling tree limbs

- Hail damage

- Flooding

- Animal collisions

Comprehensive coverage is often misunderstood because it does not mean “everything is covered.” It specifically refers to covered non-collision events.

What Is “Full Coverage” Car Insurance?

“Full coverage” is not actually a formal insurance category.

Most people use the phrase to describe a policy that includes:

- Liability insurance

- Collision coverage

- Comprehensive coverage

Some policies may also include:

- Uninsured motorist coverage

- Rental reimbursement

- Roadside assistance

- Medical payments coverage

The exact meaning varies depending on the insurer and policy.

Uninsured and Underinsured Motorist Coverage

Not every driver on the road carries enough insurance.

Some drivers:

- have no insurance

- carry only minimum limits

- let policies lapse

Uninsured or underinsured motorist coverage may help protect you if another driver cannot fully pay for damages they caused.

This type of coverage can become especially important in serious accidents involving injuries.

What Is a Deductible?

A deductible is the amount you pay out of pocket before certain insurance coverage applies.

For example:

- If your deductible is $500

- And your covered repair bill is $3,000

- Your insurer may pay $2,500

Higher deductibles often lower monthly premiums. Lower deductibles usually increase premiums.

What Auto Insurance Usually Does NOT Cover

Policies vary, but auto insurance often does not cover:

- Intentional damage

- Normal wear and tear

- Mechanical breakdowns

- Racing activities

- Driving for certain commercial uses without proper coverage

- Fraudulent claims

Always read the actual policy language carefully.

What Happens If You Drive Without Insurance in West Virginia?

Driving without insurance can trigger both administrative and court-related consequences.

Possible penalties may include:

- Driver’s license suspension

- Vehicle registration suspension

- Reinstatement fees

- Additional penalties for repeat violations

West Virginia also electronically verifies insurance coverage through its WV Online Verification system.

Common Auto Insurance Mistakes

Only Buying the Minimum Coverage

Minimum limits may not fully protect drivers after serious accidents.

Not Understanding Deductibles

Some drivers discover after an accident that they cannot comfortably afford their deductible.

Assuming “Full Coverage” Means Everything Is Covered

Policies still contain exclusions and limits.

Failing to Update Insurance Information

West Virginia drivers are expected to keep current insurance and address information updated with the DMV.

Final Thoughts

Auto insurance is partly about legal compliance, but it is also about financial protection.

The right policy depends on:

- your vehicle

- your budget

- your assets

- your driving habits

- your risk tolerance

Understanding the basics can help drivers make better decisions before an accident happens — not after.

As this insurance guide expands, we’ll also cover:

- uninsured drivers

- claim denials

- accident lawsuits

- comparative negligence

- settlements

- personal injury claims

- homeowners and renters insurance

- life insurance issues